6 Startups, 4 Exits, 28 Years: The Framework Behind Peter's Serial Wins

The exact frameworks Peter Hwang used to build, time, and exit across four very different industries.

Before we dive in, a quick note for the founders reading this.

If you have traction but no repeatable growth, if something feels stuck and you can’t quite name what, today’s guest writes the newsletter you’ve probably been looking for.

Peter Hwang is a 5x founder with 4 exits (8 and 9-figure exits) across 28 years, now investing and building his 6th startup (Tre’dish). The Unstuck Entrepreneur is where he helps middle-stage tech founders figure out what’s broken before it costs them years and resources.

Each week he publishes startup diagnoses (what's actually keeping a company stuck), Dear Founder letters, breakdowns of the determinants of founder success, and personal stories and frameworks from inside the build when you're in the quiet middle.

If this resonates, consider subscribing.

🎧 Listen to the full episode:

Spotify · Apple Podcasts · Amazon Music

Most founders build one company their entire career.

Peter Hwang has built six. Four exits. Two of them life-changing — a private equity sale and a cannabis IPO that hit close to $800 million in peak valuation before being acquired by Molson Coors Hexo for $350M.

What’s unusual about Peter’s track record is not just the outcomes.

It’s the breadth: food, finance, fundraising platforms, cannabis, groceries. Five completely different sectors. No two exits structured the same way.

When I asked him how he thinks about this, his answer was simple: he doesn’t think about sectors at all. He thinks about problems.

And he applies the same framework every time.

Here’s what that framework actually looks like.

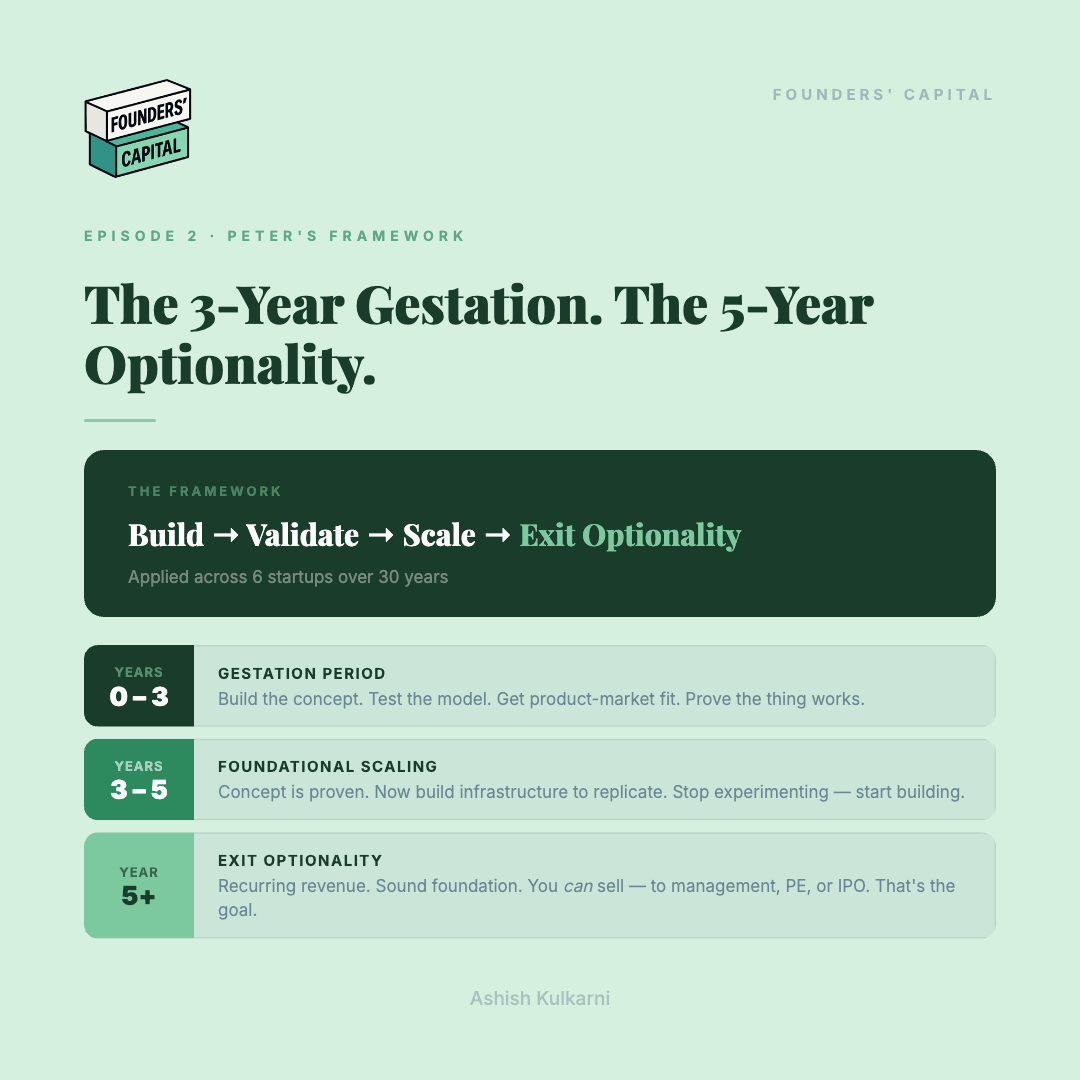

The 3-Year / 5-Year Framework

Peter calls years 0-3 the “gestation period.” This is the phase where you are not trying to scale.You are trying to answer one question: does this actually work?

In his words:

“You are trying to build out the concepts. You’re tryingto build the operational model. You’re trying to get the product market fit, see if it works. And then you have signaling that — okay, after three years,my actual concept works.”

This framework wasn’t born in a boardroom; it was born in the wreckage of 2008. Peter had built a high-performance machine - a $15 million run rate and a term sheet to go public by year two. The business was undeniably sound, but it was exposed. When the global markets collapsed, Peter realized he had built for momentum without building for durability. He had a world-class engine but no defensive layers for an "Act of God" scenario. Because he had focused entirely on the IPO path, the crash didn’t just kill the deal; it wiped out every cent he had banked from his previous two exits. He didn't lose because the business failed; he lost because he didn't have optionality. The 5-year window exists today so that Peter never finds himself at the mercy of a single exit path again.At the end of year three, you should have:

→ Proof of concept (POC) — the thing works

→ Product-market fit — people want it and are paying for it

→ Repeatable unit economics — you can model what happens at scale

If you don’t have these three things at year three, you’re either in the wrong market, solving the wrong problem, or the timing is wrong.

Years 3-6 are what he calls the “foundational scaling phase.”

This is when you’ve validated the concept and now you’re building the infrastructure to replicate it. You’re not experimenting anymore.

You’re building.

After year 5 (sometimes year 6), you enter “optionality.” This is the most important word in his framework. Optionality doesn’t mean you’re selling. It means you’ve built something stable enough that you COULD sell — to management, to private equity, or via IPO — if the right conditions appear.

“It doesn’t mean you’re selling your company. But you’ve built a company that is really sound, has likely recurring revenue, and it’s at a point where you have the option to sell it.”

The mistake most founders make: they treat exit as an event.

Peter treats exit as a state you prepare for, regardless of whether you ever use it.

Are you a founder with a story worth telling? Apply to be a Featured Founder on The Founders’ Stack.

The Four Exit Types

Peter has experienced all four main exit types across his startups.

Here’s how he thinks about each:

1. MANAGEMENT BUYOUT (Startups 1 and 2)

When to use it: When the business is a lifestyle business — good recurring revenue, but limited scalability. Your partner or team has more conviction in it than you do. What Peter did: Sold his Easy Lease portfolio to his partner.

Ceiling: “These were never destined to have a big liquidity event.”

2. PRIVATE EQUITY (Startup 4: Global Faces)

When to use it: When you have strong recurring revenue, data assets, or a defensible market position that makes you attractive to a financial buyer who wants to hold and grow.

What Peter did: Global Faces had 40 charities, 30 offices, ~1,000 fundraisers, and proprietary data on 200,000 daily impression points. PE loved the data moat as much as the revenue.

Ceiling: “Mid eight figures” — his first life-changing exit.

3. IPO (Startup 5: Newstrike / Cannabis)

When to use it: When you are in a fast-moving, politically visible sector where public markets offer premium valuation and you need capital to move faster than PE can fund.

What Peter did: Canada’s federal cannabis legalization created a unique window — companies were going public in Canada that couldn’t list anywhere else. First mover advantage mattered enormously.

“We raised $170 million off two financings within a year.”

Most founders never see a single $170M round. Peter has lived through raising it, managing the hyper-growth that follows, and eventually unwinding the complexities of a $350M acquisition.

What to watch for: IPOs require market timing. Newstrike went public at close to $800M valuation and sold to Hexo roughly two years later.

The window was real — but narrow.

4. STRATEGIC ACQUISITION (also relevant to Newstrike)

When to use it: When a strategic buyer values your company at a premium to financial buyers because of synergies, market position, or regulatory value.

Molson Coors / Hexo paid for distribution reach and licensing.

The Fundraising Formula — “The Four Walls Theory”

For early-stage fundraising (pre-seed / seed), Peter uses what he calls the “four walls theory.”

The core question: Does your problem extend beyond four walls?

What he means: Is your addressable market large enough that your solution can realistically reach beyond one geography, one demographic, or one use case? If yes — you have something pitch-able.

The formula he looks for:

Big problem × Four walls (scale beyond one context)

+ Sound deployment strategy (ICP + repeatable pilot process)

+ One-to-one proof point

= Fundable seed pitch

He’s explicit: “Ideas, everyone has a good idea. But the idea combined

with the execution of how you actually execute against it is really,

really critical.”

What he wants to see:

→ How you’re running your pilot test

→ How you’re validating with a small cohort first

→ How that cohort result maps to a larger ICP

If it has that one-to-one correlation — the problem is big enough, the four walls are extended big enough, you have a framework to start small and develop a repeatable process — then you have your recipe.

The Fundraising Progression

Peter is clear on how the stages work:

STAGE 1 — Pre-seed / idea stage:

Raise from friends, family, and high-net-worth individuals within your existing network.

“For first-time founders, that probably is where you raise your first funds.”

Exception: if your idea is so cutting-edge it can attract strangers — but he’s realistic: “There are so many ideas similar to that out there.”

STAGE 2 — Seed / POC stage:

Now you have metrics. CAC, LTV, revenue run rate, customer count. This is when you approach angels and early-stage institutional investors.

“Build some good metrics, good financials, then for the next round approach actual investors.”

STAGE 3 — Series A and beyond:

Your network from previous exits becomes a compounding asset.

“They have networks as well. It becomes a ripple effect.”

On cold outreach: Peter is direct. “Everyone is using Apollo and the same

cold email templates. If I look at my LinkedIn DMs, I probably get one

twice a day from people looking for money.”

Cold outreach barely works anymore. Warm introductions dominate.

The New Economics Of Early-Stage Building

This is where Peter’s framework intersects with the current moment.

His parting advice to founders: do more with less.

“With AI and the tools, you can now build something out with

significantly less money and less friction. The fundraising landscape

has changed because the expectation is that you should be doing

a lot more with a lot less.”

What this means practically:

→ Your POC no longer requires five technical co-founders

→ Your MVP can be built at a fraction of 2018 costs

→ You can get to proof-of-concept before you raise

→ This changes what investors expect to see at seed stage

The formula for the new fundraising environment:

Raised less money → got to POC faster → stronger seed deck

> Raised more money → longer runway → weaker proof point

“It’s not a definitive science anymore. Before it was, now it’s more

of an art — because literally you can build a pretty big company

with very little tools and little resources.”

Co-Founders And Capital Structure

One counterintuitive thing Peter said about co-founders: don’t label them early.

“Anyone that comes in at early stage — you don’t know who your co-founders are. And to put a label on them day one, before you have any POC or product market fit, is a mistake.”

Why this matters for cap table structuring:

If you give co-founder equity to people who leave in year one (what Peter calls the “uncertain middle”), you’ve diluted your cap table for nothing. Peter’s approach: let co-founders reveal themselves through behavior, not designation.

“Your co-founders actually come out of the woodwork. You realize who they truly are because they stick around.”

This isn't theoretical advice; it’s the hard-won perspective of an operator who has navigated high-stakes cap tables six different times. He has seen firsthand how early labels can paralyze a company when the "uncertain middle" arrives.

Peter felt the sting of this lesson during the early days of his current venture, Tre’dish. In the beginning, several individuals were labeled as “co-founders.” But as the “uncertain middle” set in-the grueling process of rebuilding a broken supply chain-those same people walked away. The scar wasn’t just the loss of partners; it was the psychological weight of carrying the vision alone while realizes he had diluted the company’s identity for people who were only there for the “clarity” of the start, not the friction of the build.

His rule of thumb: equal equity for equal co-founders who have equal responsibility and have earned the title. His best-performing company (Global Faces) had four equal co-founders. His worst experience came when co-founders left mid-journey.

The 30-Year Compounding Insight

The through-line of Peter’s career isn’t any single strategy. It’s the compounding of learning across failures and exits.

His first two exits were small. “Learning experiences.”

His last two were life-changing. “Global Faces and Newstrike. Those are my life-changing exits.”

What changed wasn’t the market. What changed was the framework he had built, refined, and tested across 20+ years of staying in the game.

“Stay in the game long enough. Your experience becomes far more incremental. You can actually build really great businesses. So it’s not cliche. I’ve done it over 28 years.”

The capital lesson is this: time in the game is itself a compounding asset. Not because the odds get better, but because you get better.

It’s not a dramatic answer. It doesn’t make a great reel. But it might be the most honest thing you’ll ever hear about what entrepreneurship actually requires.

Are you a founder with a story worth telling? Apply to be a Featured Founder on The Founders' Stack.

⚠️ THE FULL PLAYBOOK IS 60 MINUTES LONG...

We only had space for a few excerpts from Peter’s frameworks here. In the full conversation, we go deep into the “Investor Mindset” and exactly how Peter is currently disrupting the grocery supply chain with Tre’dish.

Don’t miss the full configuration. Catch the 60-minute deep dive here:

Spotify · Apple Podcasts · Amazon Music

Best,

Ashish

| A guest post by

|