From Russian Oil Fields to US Runways. The Business Case for Universal Fuel Technologies.

Universal Fuel Technologies is raising a Series A. Here is what the numbers say and what Alexei Beltyukov said when we sat down with him.

This week on The Founders Stack we sat down with Alexei Beltyukov, CEO and co-founder of Universal Fuel Technologies. We covered a lot of ground in that conversation, most of it psychological. But sitting underneath the personal story is a business that has been quietly developing since 2006 and is now at a genuinely interesting commercial inflection point.

Are you a founder with a story worth telling? The Founders Stack is looking for founders who are willing to go beyond the highlight reel and talk honestly about what building has actually cost them. If that sounds like you, we would love to hear from you.

This piece is the Founder’s Capital side of that conversation. The technology, the market, the team and what the pitch deck tells us about where they are and where they are trying to go.

The full podcast is on The Founders Stack YouTube channel. This podcast focuses more on the Founders’ Psyche side, going ahead I might have people with whom I can focus more on Founders’ Capital. Link below:

If you prefer other platforms click - Spotify , Apple Podcasts, Amazon Podcasts.

What the Technology Actually Does

Universal Fuel Technologies (unifuel.tech) is a chemical technology startup licensing Flexiforming®, a catalytic process that converts low-cost feedstocks into sustainable aviation fuel (SAF), high-octane gasoline, and BTX. With 27 granted patents and a commitment to fund our First-of-a-kind plant by a US oil refiner, UFT is commercializing one of the most capital-efficient pathways to renewable fuels.

You can view the full pitch deck of UFT below for FREE!

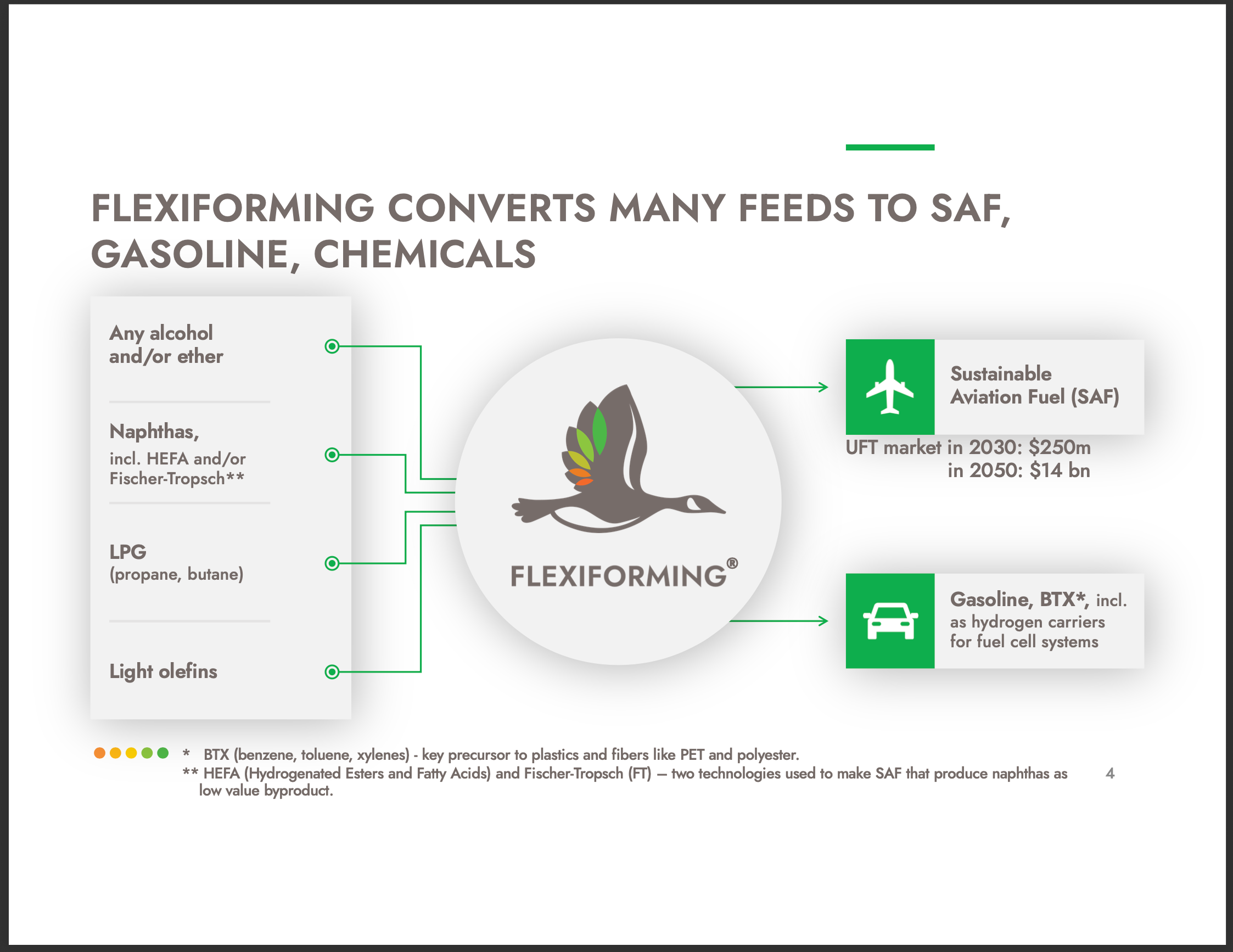

Universal Fuel Technologies is built around a proprietary process called Flexiforming. At its core it is a catalytic conversion technology that takes a wide range of feedstocks, alcohols, ethers, naphthas, LPG, light olefins, and converts them into higher value outputs including Sustainable Aviation Fuel, high octane gasoline and specialty chemicals like BTX, which is a key precursor to plastics and fibres.

The key word in that description is flexibility. Most fuel conversion technologies are designed around specific feedstocks. Flexiforming is not. It was built to work with whatever is available, which is exactly why it translates so well into renewables where feedstocks are fragmented, location dependent and rarely consistent.

In an emergent market like Russia, if you do something and you’re somewhere close to what the market wants, you’re okay. In the US, you have to be exactly on point. If you’re off by a millimeter, you’re out of money.

That observation from Alexei in our conversation captures something important about what Flexiforming is trying to do in the US market. The SAF space is not forgiving. Airlines need to meet certification standards, producers need to hit cost targets and the technology has to work reliably at varying scales. UFT’s pitch is that Flexiforming does all three better than the dominant alternatives.

According to their deck, the cost of Flexiforming SAF sits within 50% of the price of fossil jet fuel and unlocks up to 35% additional margin for SAF producers compared to the existing standard process. More than 95% of SAF today is made using HEFA, which is expensive and feedstock constrained. Flexiforming opens up the feedstock base considerably.

The Market Opportunity

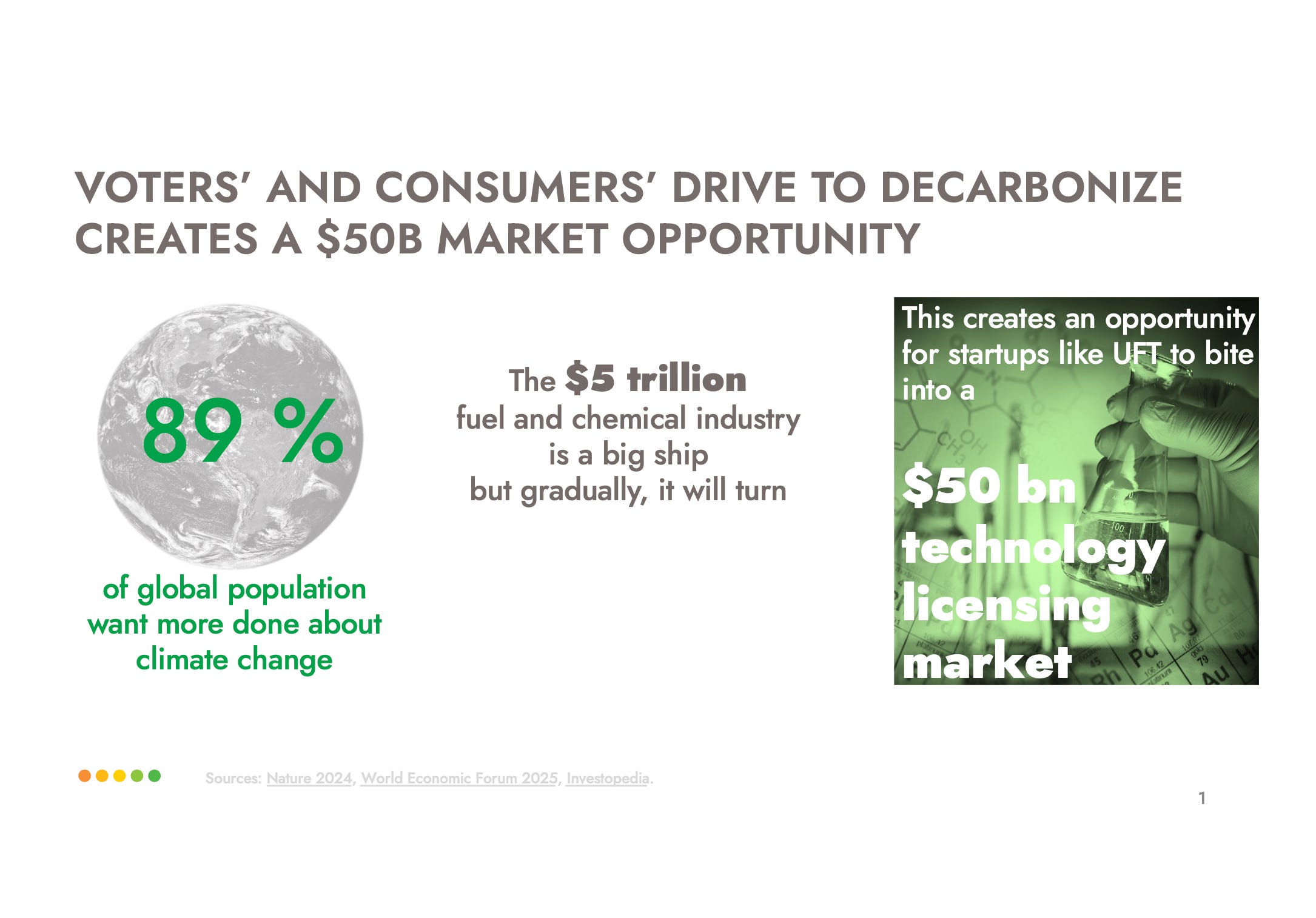

UFT is going after what their deck describes as a $50 billion technology licensing market sitting inside a $5 trillion fuel and chemical industry. Their own addressable market projections are more specific: $250 million by 2030 and $14 billion by 2050, driven primarily by SAF mandates coming into force across the US and Europe.

The SAF market has genuine structural tailwinds. Airlines in Europe are already subject to blending mandates and the US is moving in the same direction. The problem has never been demand, it has been cost and supply. Every airline wants to buy SAF. Very few can afford to at current production costs. That is the gap UFT is positioning into.

What makes their market entry interesting is the business model. They are not building refineries. They are licensing the technology and selling the proprietary catalyst that makes it work. The deck describes it as a razor blade model, the technology licence is the razor, the catalyst replacement every few years is the blade. Gross margins on licensing sit at 95% and the blended EBITDA margin across all three revenue streams, licensing, catalyst and engineering services, is projected at 60%.

Development never stops. You stop development every day. Client-wise, we just got a client commit to a project with us, a US-based client. So that’s what we’re busy with right now. And there are a few more in the pipeline.

The customer pipeline in the deck is detailed and spans North America, Europe and the Middle East. First year revenue potential across the full pipeline is listed at $250 million. Most of the final investment decisions are clustered between 2026 and 2028, which tells you the near term commercial priority is getting the first few plants operational and generating reference cases for the rest of the pipeline.

The Team

The team slide is one of the stronger parts of the deck and it is worth looking at carefully. Alexei brings three profitable exits including one at 30x in the energy and chemicals space. His co-founder Denis Pchelintsev is the engineering backbone with 35 patents related to fuel chemistry and production. Stephen Sims, VP of Business Development, spent over 30 years at major US oil refineries including as a Technical Manager and has sold two technology licensing businesses of his own.

That last detail matters more than it might look. Selling a technology licence to an oil refinery is not like selling software. The buyer is deeply technical, highly risk averse and has been burned before by technologies that worked in a lab and failed at scale. Having someone on the team who has sat on the buyer side of exactly this transaction, multiple times, is a genuine commercial advantage.

The deck notes the core team has been together for eleven years and describes them as having a playbook. Given the technology has already been through a full commercial cycle in Russia, including four operating plants, that claim has some evidence behind it.

Where They Are in the Journey

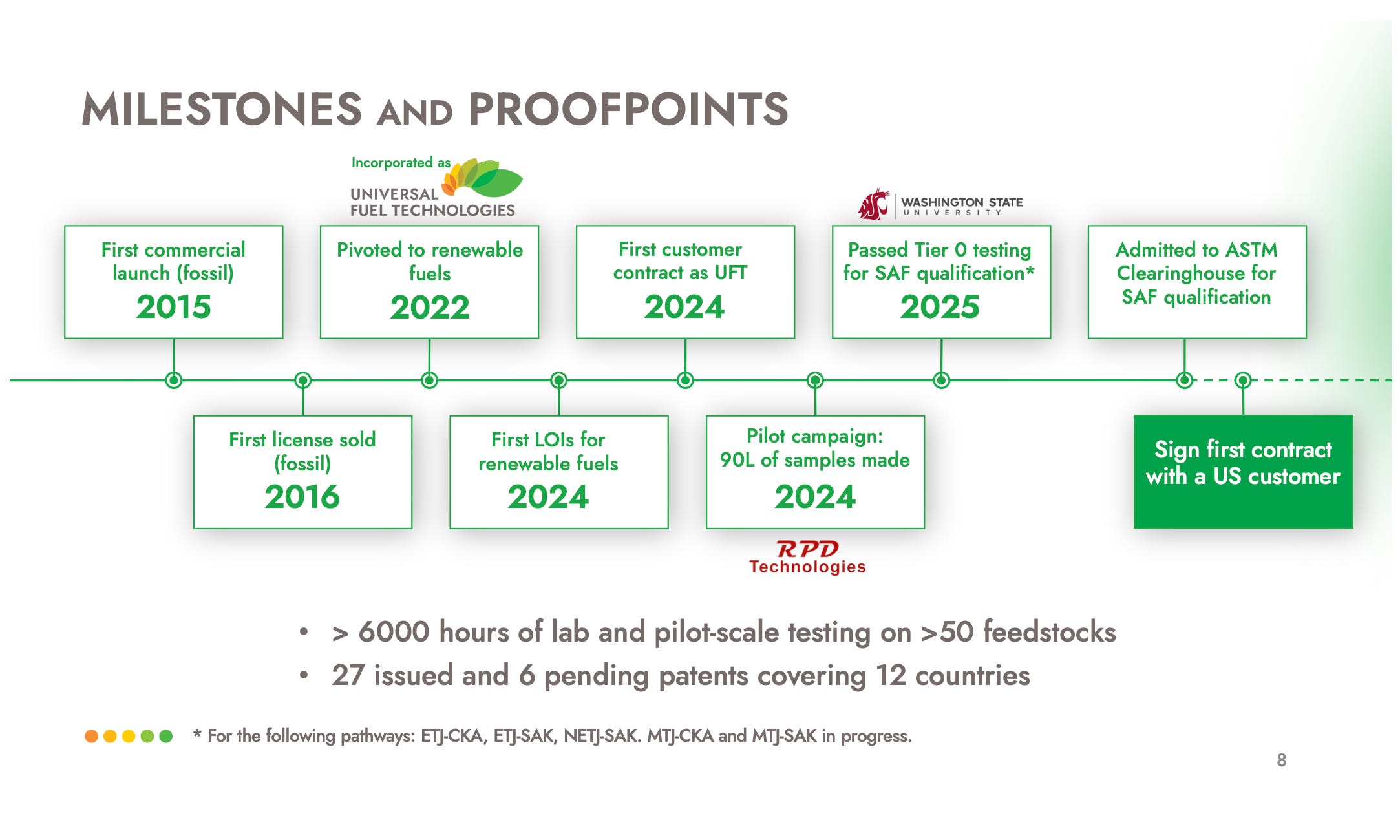

The milestone timeline in the deck is one of the most honest parts of the presentation. First commercial launch was 2015. Pivot to renewables came in 2022, forced by the war in Ukraine. First customer contract as UFT was 2024. SAF certification testing at Tier 0 passed in 2025 with Washington State University. Admitted to the ASTM Clearinghouse for SAF qualification is listed as the current milestone alongside signing the first US customer contract.

That is a ten year journey from first commercial to first US customer. A lot of that time was spent in Russia building something that the war then made unreachable. The pivot into renewables was not planned, it was forced. But as Alexei explained in our conversation, the same properties that made Flexiforming useful in Russian oil fields, flexible feedstocks, small scale efficiency, low carbon intensity, turned out to be exactly what the renewables market needed.

When the war started we thought, let’s look at what else we can do. With some nudges from our friends, we discovered this world of renewables, which we were completely oblivious to before. And it turned out our technology is ideal for renewables.

They are currently raising a Series A. The round is open. Given where they sit in the milestone timeline, between first commercial traction and full pipeline conversion, the raise is essentially about getting from proof of concept to proof of scale. The first US customer project currently underway is the reference case everything else depends on.

What to Watch

The honest question for any investor looking at UFT is execution risk on the first US plant. The technology has a track record but that track record is in Russia, with different regulatory environments, different customer relationships and different scale requirements. The US is a different game entirely, as Alexei acknowledged in our conversation.

The SAF certification pathway is also not trivial. Tier 0 testing passing is meaningful progress but full ASTM certification for a new conversion pathway takes time and the airlines that need to buy SAF at scale cannot move until that certification is complete.

On the other side of the ledger the business model is genuinely attractive. Technology licensing at 95% gross margin with a recurring catalyst revenue stream is a rare combination in hard tech. If the first US plant works as the deck says it should, the pipeline behind it is substantial and the reference case alone could accelerate the remaining deals considerably.

It is a company that has been building for a long time, through circumstances that would have stopped most teams. Whether that patience and persistence translates into commercial momentum in the US market over the next two years is the question the Series A is effectively betting on.

The full conversation with Alexei is on The Founders Stack YouTube channel. Links below.

YouTube:

See you next issue.

Ashish