What your SAFE actually does at the next round

Every SAFE has a second bill. Here's how to read it before you sign.

A founder showed me his cap table this week and asked me to tell him what was wrong.

He had raised three SAFEs over the last fifteen months. Each one felt fine at the time. The terms were standard. The caps were reasonable. The investors were respected. He was about to close his Series A and his lawyer had just sent him a model showing his post round ownership at 58 percent. He thought he would land closer to 65 percent. He wanted to know where the seven points went.

The seven points went where most founders never look. They went into the second order effects of the SAFE math. Not the headline conversion, which most founders learn to model. The compression that happens after the SAFE converts, which almost no founder models.

This piece is for the founder who is about to sign a SAFE or about to price a round on top of a SAFE stack. It walks the math in three parts. The conversion. The compression. The questions to ask before signing.

The Conversion

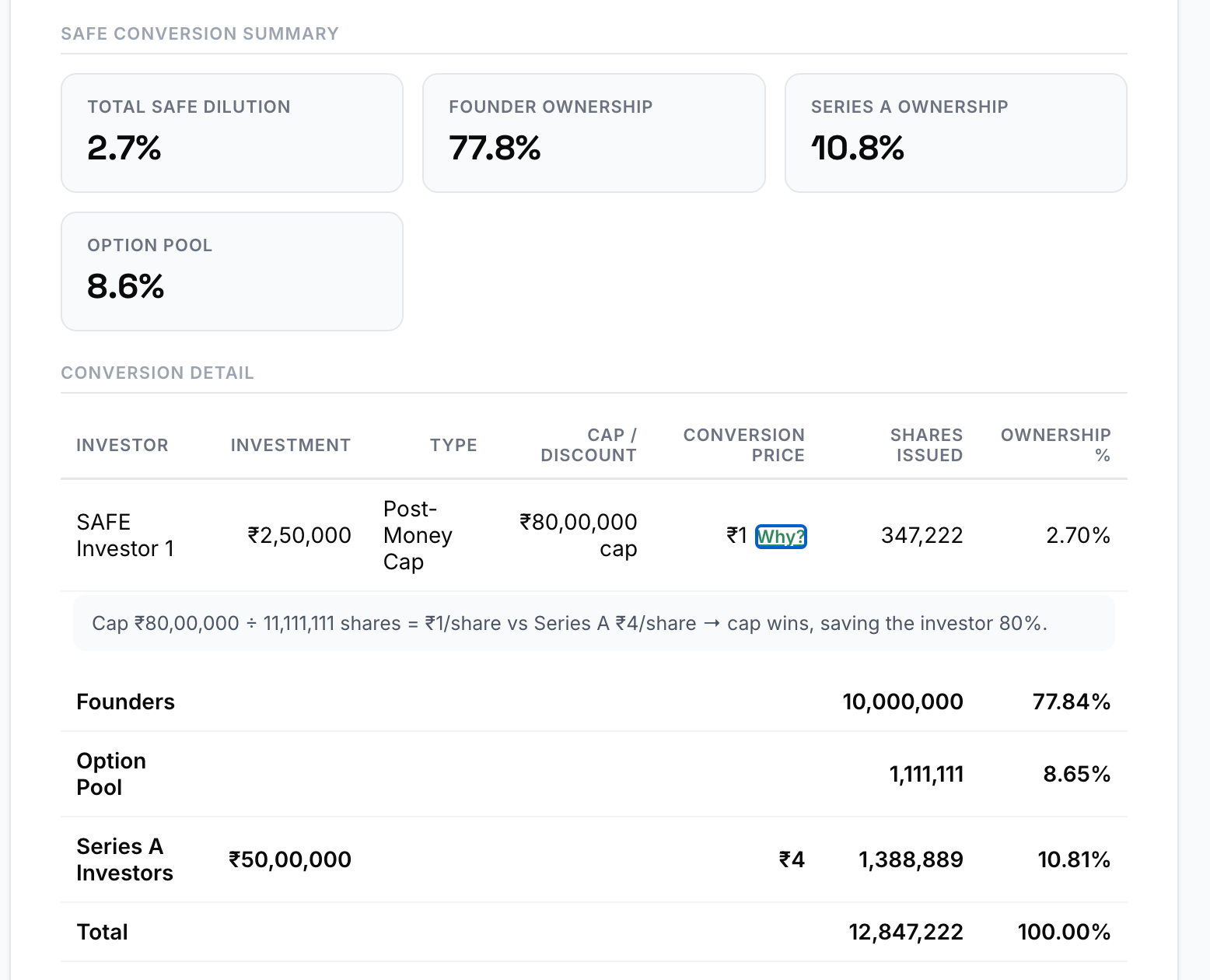

A SAFE has a cap and sometimes a discount. When a priced round happens at a price above the cap, the SAFE converts at the cap. When the priced round is below the cap, the SAFE converts at the priced round (with the discount applied if relevant). Most founders understand this much.

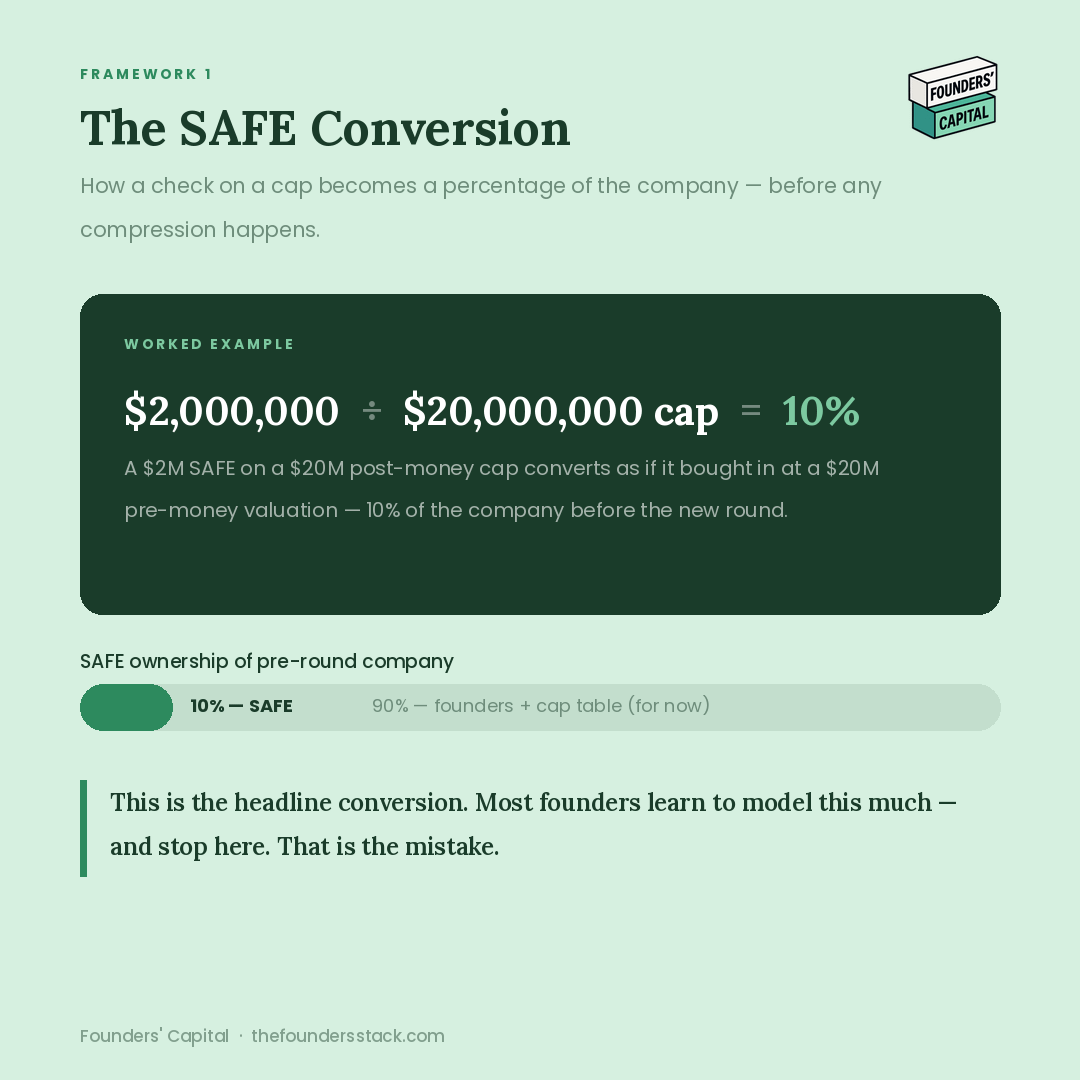

Worked example. You raised 2 million on a SAFE with a 20 million post money cap. Your next round prices at 25 million post. The SAFE converts as if it bought at a 20 million pre money cap. The SAFE ownership is 2 divided by 20, which is 10 percent of the company before the new round.

If you stopped the math here you would walk into the Series A confident that the SAFE took 10 percent and the new round would take its own slice on top. You would also be wrong about your end state by two to three percentage points.

The Compression

Here is the part that breaks most founders.

The Series A investor wants 20 percent of the company after the SAFE converts. They do not care what the SAFE took. They are pricing the round on a fully diluted basis that includes the SAFE conversion plus an option pool top up.

The SAFE shares come in before the Series A shares. So the order of operations is. SAFE converts. Option pool tops up. Series A buys 20 percent. By the time the Series A is in, the SAFE and the option pool have both already compressed the existing cap table.

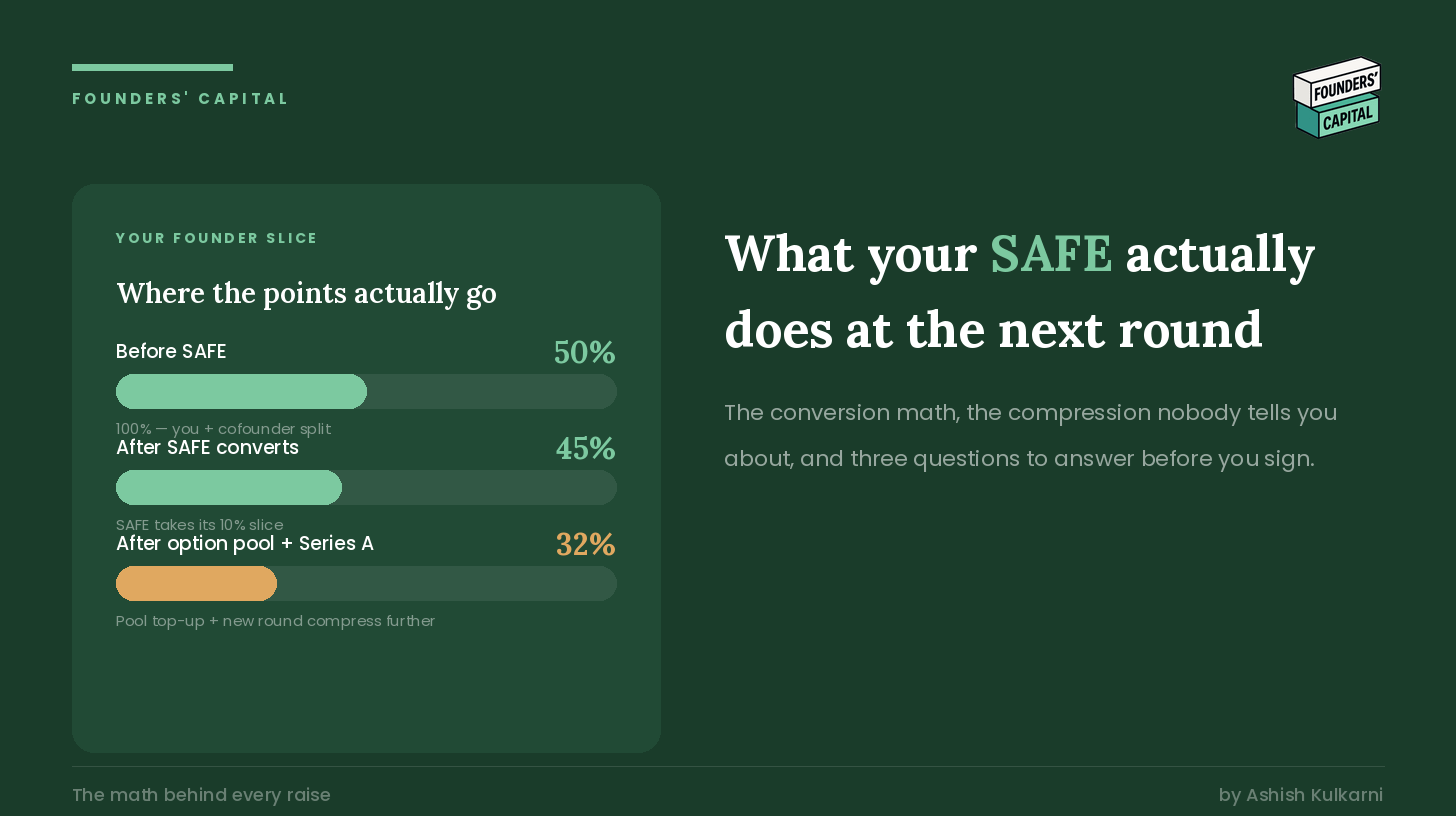

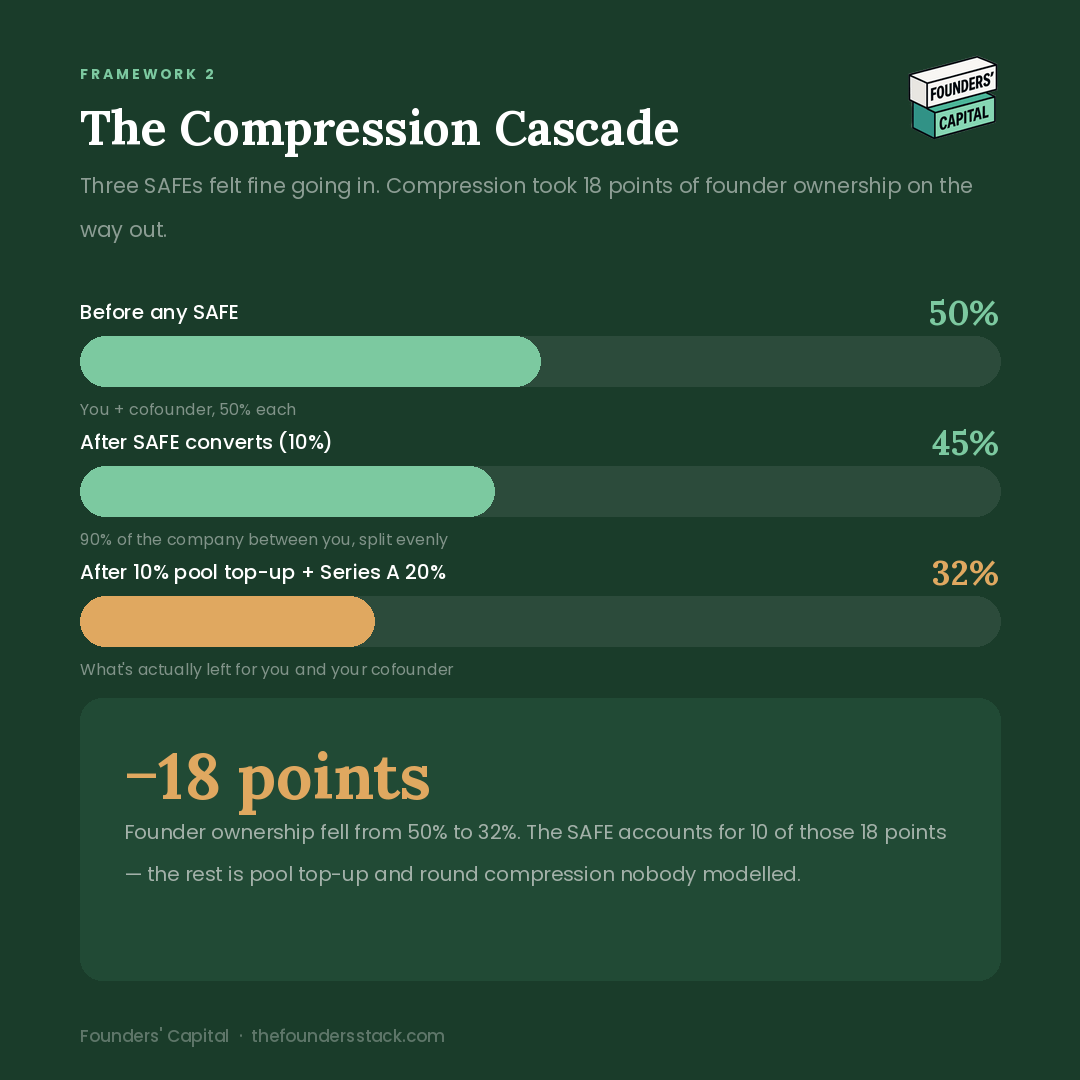

In the 2 million on a 20 million cap example. Your starting cap table was you and your cofounder at 50 percent each. After the SAFE converts you are at 45 percent each (90 percent of the company between you, 10 percent to SAFE). If your Series A investor wants 20 percent post money and the lead also wants a fresh 10 percent option pool, the math compresses you and your cofounder further. You both end up around 32 percent. Not 40. Not 38. Around 32.

Your starting position was 50 percent. Your end position was 32 percent. The SAFE you thought took 10 percent took closer to 18 percent of your personal slice because of how the pool top up and the priced round stack on top of it.

This is the seven points the founder above could not find. They were never lost. They were spread across three SAFEs each compressing slightly more than the headline conversion suggested.

The Questions to Ask Before Signing

Three questions every founder should answer before signing a SAFE. If you cannot answer them in numbers, you are not ready to sign.

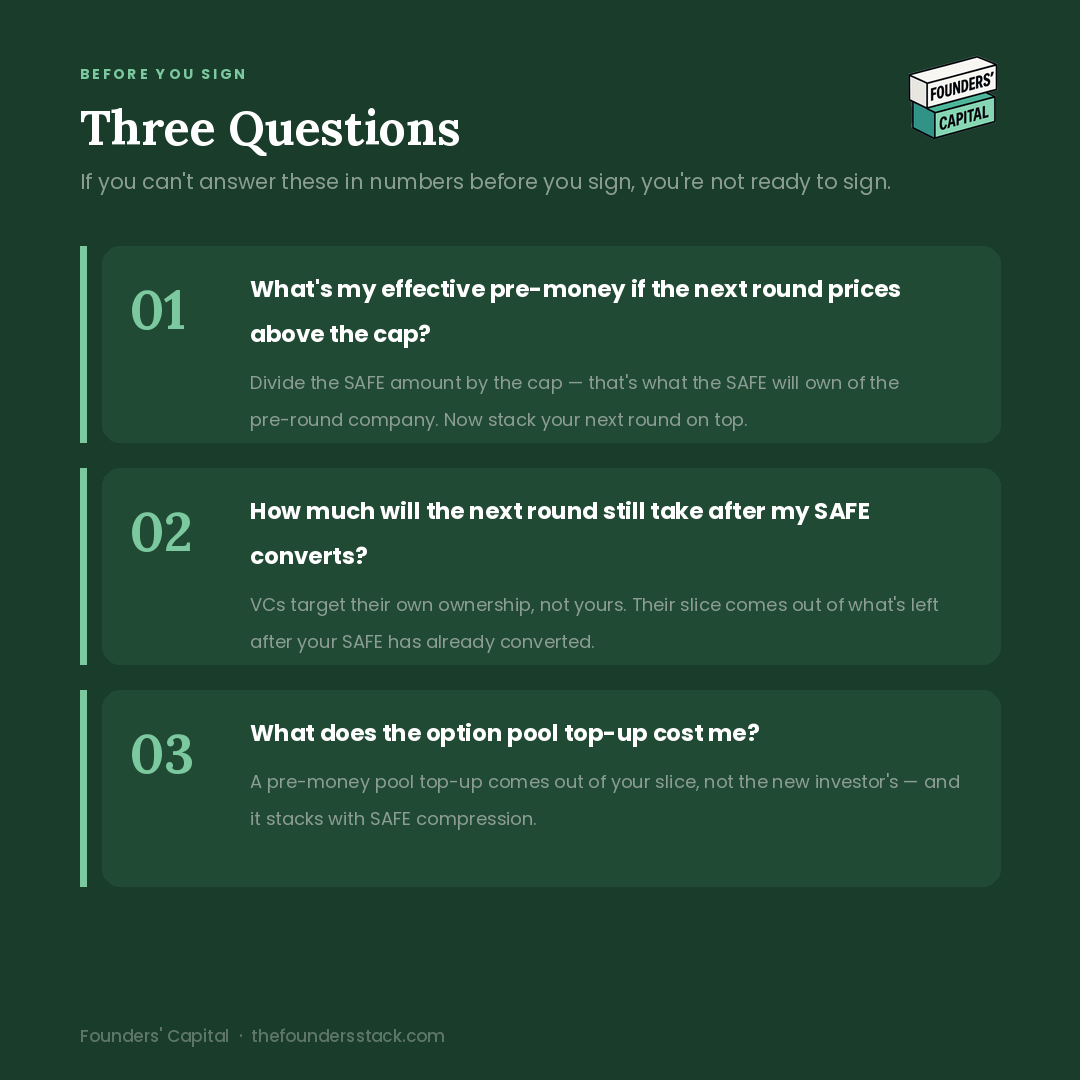

1. What is the effective pre money if my next round prices above the cap? Take the SAFE amount and divide by the cap. That is what the SAFE will own as a percentage of the pre new round company. Now imagine the new round on top of it. Where does your slice land?

2. How much will the next round still need to take after my SAFE converts? VCs do not budget around your SAFE. They budget around their target ownership. If your Series A lead wants 20 percent, that 20 percent comes out of the company after your SAFE has already converted. Your SAFE compresses your slice. Their 20 percent compresses what is left.

3. What does the option pool top up look like at the next round? Most term sheets include a pre money pool top up that comes out of your slice, not the new investor’s. A 5 percent top up on a 25 million post round is another 1.25 percent that comes out of your personal stake before the new round prices. Combined with the SAFE compression, this is where the most invisible dilution lives.

The founders who lose the most equity are not the ones who took bad terms. They are the ones who took fine terms without doing the math. A 20 million cap is fine. A 1 million discount is fine. A 5 percent pool top up is fine. Stack three of them and run them through one priced round and the founder slice can drop ten points before the new round even fully closes.

This is fixable. None of this math is hard. What is hard is making the time to model it three rounds out before signing the first one. Most founders model the round they are in. Almost none model the round they are walking into.

A simple discipline that costs nothing. Before signing any SAFE, build a scenario where your next priced round prices flat, at the cap, and at twice the cap. Run the math in all three scenarios. See what your slice looks like in each. If you cannot live with the worst of the three, do not sign.

This is also the discipline TermLab tool in The Founders’ Stack is built around. You enter your existing cap table, add the SAFE you are about to sign, and the model surfaces all three scenarios with full waterfall math. Nothing fancy. Just the math, run faithfully, before the signature instead of after. Run your own numbers before you sign.

The founder who showed me his cap table this week did not have a deal problem. He had a math problem. He had been signing fine terms three rounds ago and never doing the math forward. The terms compressed when the priced round arrived and by then the math was done.

You can do this work. You can do it before the signature instead of after. You can stop being the founder who finds out at the Series A what the seed actually cost.

The math is not the obstacle. The discipline is.

Best,

Ashish